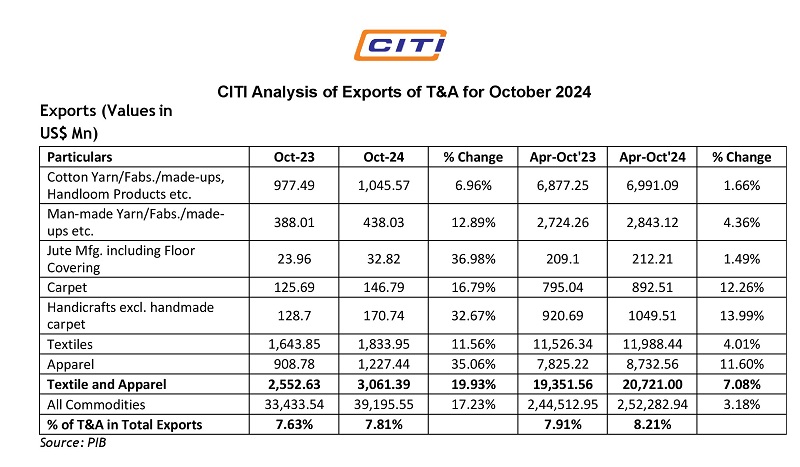

The apparel industry in Asia presents a fascinating picture of contrasting fortunes. While Bangladesh, Vietnam, and Sri Lanka have seen their garment exports soar in recent years, India, a traditional powerhouse in textiles, struggles to keep pace. This analysis delves into the reasons behind this disparity and explores potential solutions for India to reclaim its export dominance.

Why India lags behind

|

Country |

2021 ($ billion) |

2022 ($ billion) |

2023 (estimated, $ billion) |

|

|

India |

30.5 |

29.8 |

29 |

|

|

Bangladesh |

42.6 |

45.7 |

48 |

|

|

Vietnam |

39.7 |

44.4 |

48.5 |

|

|

Sri Lanka |

6.1 |

6.8 |

7.2 |

Despite having a strong domestic cotton industry and a large workforce, India's apparel exports are losing ground. Several factors are responsible for this.

Productivity gap: Bangladesh and Vietnam boast of higher productivity due to several factors.

Specialization: These countries focus on specific garment segments, allowing for efficient production lines and skilled workers. India's broader product range can lead to inefficiencies.

Investment in automation: Bangladesh and Vietnam are actively adopting automation technologies for cutting, sewing, and packaging, leading to faster turnaround times. India lags in this area. These investments and streamlined production processes, lead to higher output per worker. India's garment industry remains fragmented, with many smaller players relying on less efficient technologies.

Labor cost advantage: While wages are rising across Asia, Bangladesh still offers a significant cost advantage compared to India. This attracts buyers seeking value-driven apparel. Often perceived as having a labor cost advantage, India's edge is diminishing. Although base wages might be lower, factors like complex regulations, fragmented infrastructure, and lower skill levels can negate the cost benefit.

Table: Average Monthly Garment Worker Salary ($)

|

Country |

Salary |

|

Bangladesh |

190 |

|

Vietnam |

230 |

|

India |

250 |

Emerging market focus

There's a silver lining. While traditional markets like the US and EU remain important, a shift towards emerging markets like Southeast Asia and Africa presents an opportunity for India. These regions offer potential for growth due to rising disposable incomes and a growing middle class. All four countries are looking to tap into these new markets with their growing middle class and rising apparel demand.

Table: Export destinations

|

Country |

Traditional Markets (US & EU) |

Emerging Markets |

|

India |

65% |

35% |

|

Bangladesh |

70% |

30% |

|

Vietnam |

60% |

40% |

|

Sri Lanka |

80% |

20% |

The road ahead for India

To regain its competitive edge, India needs a multi-pronged approach. First, it needs to invest in skill development. Upgrading worker skills through targeted training programs can significantly boost productivity. Second is focus on modernizing infrastructure. Streamlining logistics and reducing bottlenecks can improve efficiency and lead times. Third, focus on automation as embracing automation in specific areas can help bridge the productivity gap.

And fourth, moving beyond basic garments and focusing on higher-value products can help India command premium prices. Fifth is streamlining regulations and simplifying labor laws and export procedures can attract investments and reduce operational costs.

India has the potential to reclaim its position as a leading apparel exporter. By addressing productivity gap, labor cost competitiveness, and focusing on strategic areas, India can capitalize on its raw material advantage and skilled workforce to regain its export dominance in the global apparel market.