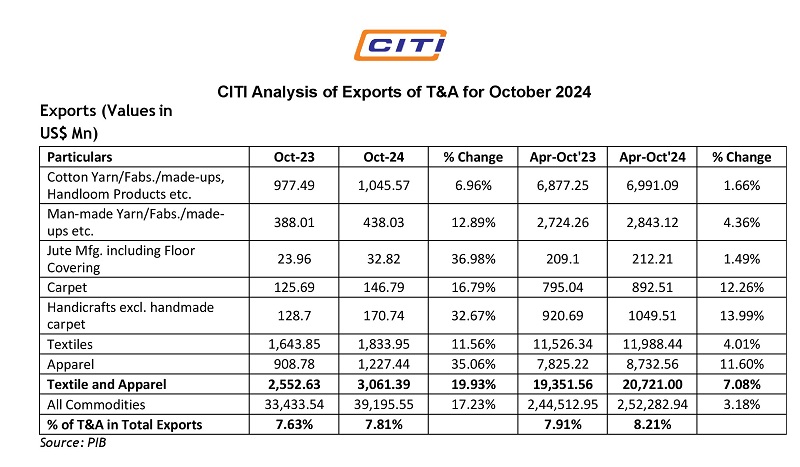

FDI boosts economy

Goel and Hong Phuc feel, investments will not only come from TPP participant countries, such as the US and Japan where booming garment and shoe industries are poised to benefit from the elimination of tariffs, but from any country whose manufacturers are seeking easier and more secure access to some of the world’s most exciting consumer markets.

However, keeping in mind the favourable prospects for textile and garment industry, macro-economic indicators, pose fair warning to export dependent economies such as Vietnam. This is because the TPP and other future free trade agreements (FTAs) bring opportunities to Vietnam for increasing production and export, they will also create challenges that need to be tackled to secure future economic prosperity.

The past decade saw Vietnamese GDP grow at 6 per cent plus CAGR. The conducive economic environment has helped Vietnam grow its economy from $57 billion in 2006 to $187 billion in 2014. Investors are bullish about this growth and have pumped in $4 billion into the economy annually between 2001 and 2015. The textile industry is a primary growth engine in a manufacturing-driven economy contributing 15 per cent to the overall GDP, 18 per cent to overall exports, and 4 per cent to the global textile industry.

Textile industry’s growth drivers

The duo feel Vietnam’s textile industry, being an important driver of the economy, necessitates a focus in strategy formulation to maintain robust and sustainable performance in the evolving economic scenario. The primary driver for growth of Vietnamese textile industry came about with the completion of Multi Fibre Agreement (MFA) in 2005, which resulted in the abolition of quotas for first-world exports. The abundance of orders from the developed world resulted in a spurt in manufacturing with a mushrooming of small to medium players across these countries with turnover between $50 million to $200 million per annum. With Vietnam’s share of the global textile trade at 4 per cent, and being one of the top exporters of textiles and garments to the US, there is still a lot of scope in the short- to medium-term for accommodating more companies, or for the existing ones to add significantly to their current volume and revenue.

The duo feel FTAs being signed with the Eurasian Customs Union, and South Korea, as well as the TPP (which is estimated to increase exports to the US from $9.8 billion in 2014 to $30 billion in 2020) will certainly provide this impulse. However, while the macro situation seemingly assures sustained topline growth potential, the challenge of comparative cost inefficiencies will be even more significant with general price reductions by competing countries. Statistics show that while trade has expanded, the prices from exporting nations have actually reduced. The global price reduction trends put immediate pressure on the suppliers.

Investment in technology to stay competitive

It is imperative for the Vietnamese textile industry to look deeply into its operating models and tackle possible cost disadvantages to remain competitive globally. Studies have shown that once the TPP comes into effect the new trade relationships would create an additional six million jobs in Vietnam’s textile and garment industry. However, it will also increase the labour wage by 12 to 15 per cent. As a consequence, Vietnam needs to invest in techniques of modern floor management and industrial engineering practices to further enforce the advantage. Industrial engineering, lean manufacturing practices – especially in the cut and make departments – can help the organisations increase labour productivity substantially.

Supply lead time, according to the duo, is the other major differentiator: Players having control on upstream activities would be the first choice for customers sourcing in Vietnam. Gaining control can be done either by backward integration or putting appropriate demand management, planning, and procurement processes in place. For Vietnam, a key aspect of the infrastructure, apart from the plant and machinery, is the logistics infrastructure. The current state of Vietnam’s logistics infrastructure is sub-optimal, leading to higher procurement and delivery lead times with the sourcing to free on board shipping point) time often as high as 80 days. Players in other countries are operating with lead times of between 40-50 days. The situation can be remedied through the development of local sourcing options, which can cut the sourcing time of 20 days considerably.

www.kpmg.com